42 fhlmc unemployment income

When unemployment income associated with the seasonal employment is being used as stable monthly income: A documented two-year history of seasonal employment and income receipt is required, and; The requirements for unemployment income associated with seasonal employment in Section 5303.3 must be met; Union members Income Trending: After the monthly year-to-date income amount is calculated, it must be compared to prior years' earnings using the borrower's W-2's or signed federal income tax returns (or a standard Verification of Employment completed by the employer or third-party employment verification vendor).

Income from unemployment benefits is typically short-term in nature and can be considered when qualifying the borrower in the following scenarios: The income has been consistently received for at least two years as verified by copies of the signed federal income tax returns that reflect the unemployment income is associated with seasonal ...

Fhlmc unemployment income

The Borrower's earnings may be comprised of base non-fluctuating earnings, ... When unemployment income associated with the seasonal employment is being ... Evaluating Income Amid a Pandemic. The coronavirus (COVID-19) global pandemic is challenging some potential borrowers and recent employment trends have complicated the qualifying process for borrowers who are experiencing temporary job loss because of COVID-19. Lenders have had to quickly adapt how they work with current and future homeowners ... Unemployment income must be documented for two years, and there must be reasonable assurance that this income will continue. This requirement may apply to seasonal employment. Reference: For information on analyzing income from seasonal employment, see HUD 4155.1.4.D.2.e. 4155.1 4.E.3.d

Fhlmc unemployment income. General requirements for all stable monthly income. Effective 12/01/2021 ... Unemployment (associated with seasonal employment). Self-employment income.Income types: Continuance requirement highli...Mortgage differential: Document duration of pa...Dividend and interest: Document sufficient ass...Homeownership Voucher Program (HOV): Do... • Evidence of amount and duration of all temporary income Seasonal Income • Both Fannie & Freddie standard income documentation for second jobs listed page 1 • The employer must confirm there is a reasonable expectation the borrower will be rehired • Unemployment income may be used to qualify if a two-year history on tax returns 1500: Seller Master Agreements, other Pricing Identifier Terms and Guide Plus Additional Provisions. 2000. Doing Business with Freddie Mac. 2100: Seller/Servicer Institutional Eligibility. 2200: Additional Requirements for Doing Business with Freddie Mac. 2300: Disqualification or Suspension of a Seller/Servicer. Income from commissions or self employment is considered stable when the applicant has obtained such income for at least 2 years. Less than one year can rarely qualify ... Unemployment income can not be used as qualifying income. ... FNMA and FHLMC issue a list of approved appraisers and allow the lender to choose the appraiser from the list.

Stable verified income to support a monthly payment Unemployment is considered a temporary hardship. You must consider unemployed borrowers for unemployment forbearance under Guide Sections 9203.22 through 9203.24. Unemployment benefits may not be considered a source of income for a modification. Streamlined Eligibility for Certain Borrowers The Effects of Expanded Unemployment Benefits and Stimulus on Unemployed Renters' Income During COVID-19. The COVID-19 pandemic created the most severe and abrupt economic downturn in recent history. The resulting economic disruption has left millions unemployed and reliant on unemployment benefits. Three separate rounds of federal legislation ... Forbearance is a relief option for borrowers experiencing a short-term or long-term hardship. There are different types of forbearance plans available depending on the borrower's hardship. All forbearance plans consist of a written agreement that allows the borrower to skip or reduce their monthly mortgage payment for a specified period of time. Yes, in some cases income documentation may need to be updated for self-employed borrowers. Refer to . LL-2021-03 for details. Q4. Can I use the requirements for income while on temporary leave? Certain types of temporary leave may be eligible for qualifying. See . B3-3.1-09, Other Sources of Income; Temporary Leave Income.

Freddie Mac- Unemployment Reviewing & Calculating Income from Miscellaneous Sources 32 Single-Family Seller/Servicer Guide Selling Series 5000: Origination and Underwriting Topic 5300: Stable Monthly Income and Asset Qualification Sources Chapter 5303: Employed Income 5303.3: Additional employed income (09/14/17) Temporary Leave Income. When income from temporary leave is being used to qualify for the mortgage loan, the lender must enter the appropriate qualifying income amount into DU based on the requirements provided in B3-3.1-09, Other Sources of Income. If the borrower will return to work as of the first mortgage payment date, the lender can consider the borrower's regular employment income in ... the borrower's recent paystub and IRS W-2 forms covering the most recent two-year period. (Signed federal income tax returns may also be required to verify unemployment income related to seasonal employment.) A verbal VOE is also required from each employer. See B3-3.1-07, Verbal Verification of Employment, for specific requirements. Income Annualized Unemployment Benefits + Stimulus % Difference $20,000 $25,572 37.9% $30,000 $32,786 9.3% $40,000 $38,000 -5.0% $50,000 $42,328 -15.3% Sources: Census.gov, State Employment Agencies, Freddie Mac Unemployment Benefits Compared with Median Renter Household Income by State

Will there be another stimulus check? Will federal ...

Need Help? Please contact your Freddie Mac Account Representative or the Customer Support Contact Center. +1-800-FREDDIE. Start Cobrowse Session.

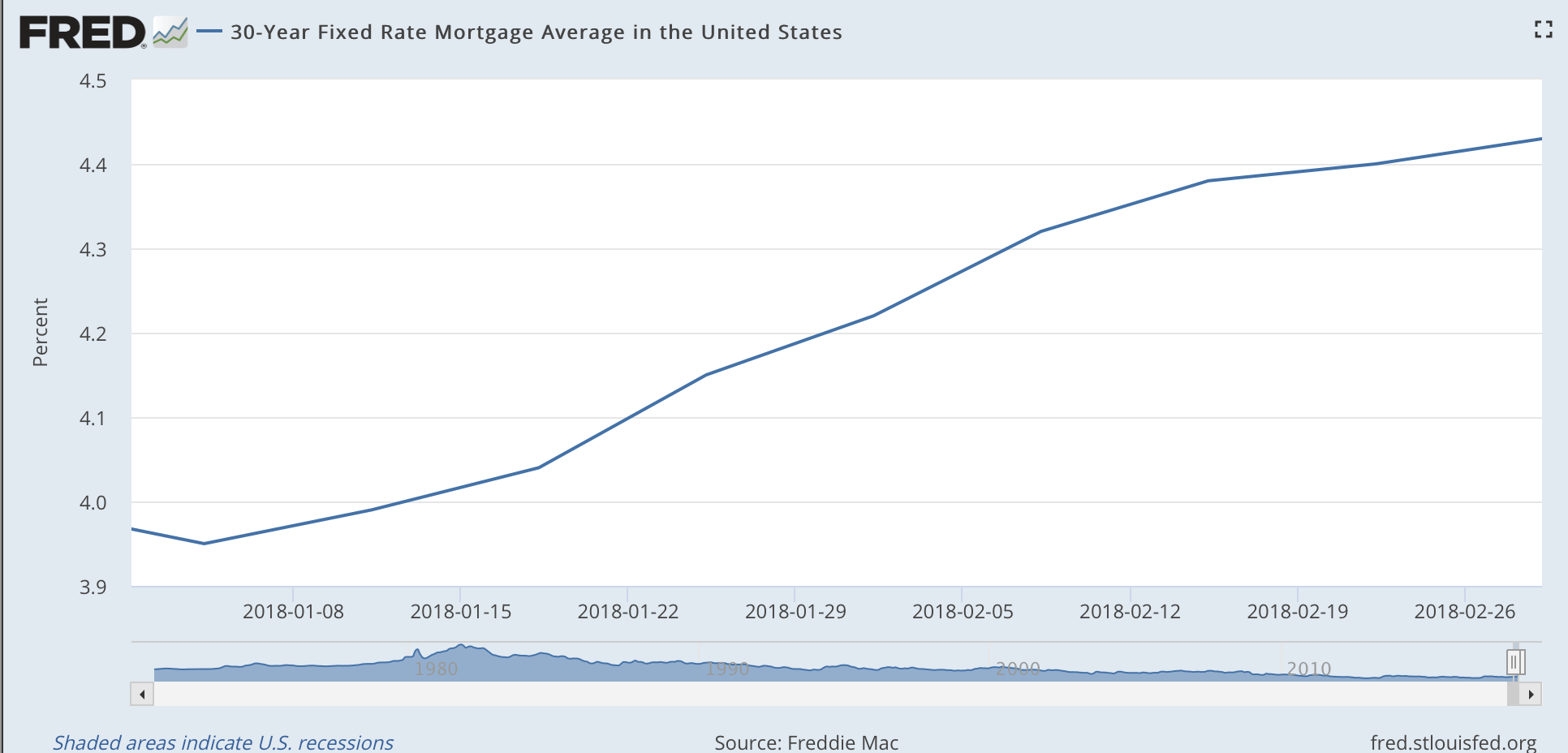

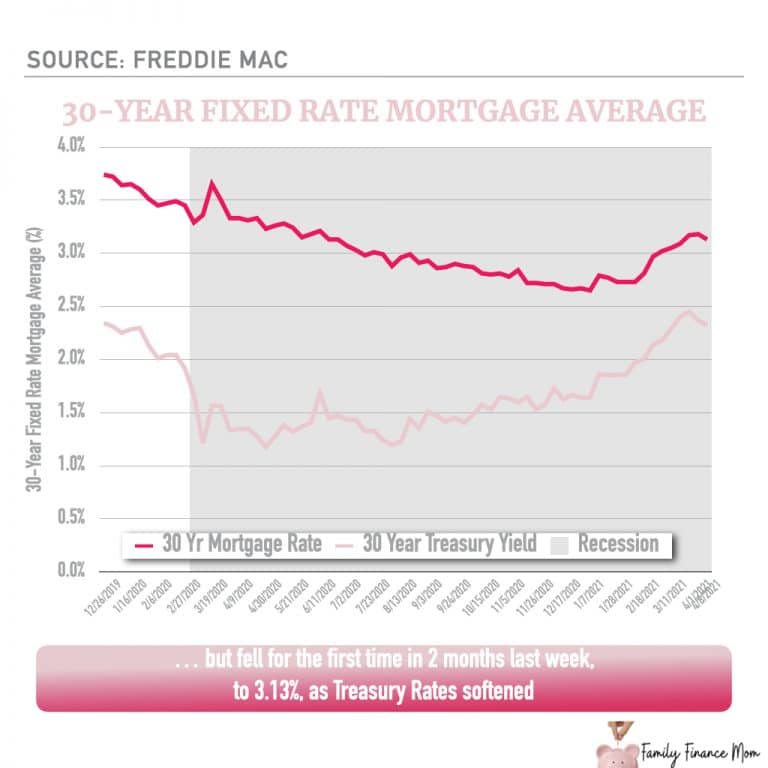

Mortgage Rates are Climbing and Inventory is Shrinking ...

Certain union members may work in industries where they may switch employers frequently and the union facilitates the next position. A Borrower may exhibit a ...

Now's The Time To Consider The Consumer Mortgage Market ...

Freddie Mac

How's the Market? (Part 2) | NorCal Partners Real Estate

May 5, 2021 — The Seller must analyze all income documentation while taking into consideration the characteristics of the employed income (e.g., employment ...

Home without a Home

Tip Income - Freddie Mac Tip income T he Borrower must have a two-year consecutiv. e history of receiving income from tips in order to consider the income for qualifying. For tip income that fluctuates, the Seller must evaluate the income trend and use the amount that is most likely to continue for the next three years

Vaultedge newsletter - Jerry Maguire or Mike Lyon? | Revue

Freddie Mac Single-Family Seller/Servicer Guide Bulletin 2021-22 Effective 06/09/21 Page E101-1 The required documentation to verify income disclosed by the Borrower(s) on Form 710, Mortgage Assistance Application, and the corresponding methods to calculate the income from each type are provided in this exhibit.

Freddie Gray case explainer - Los Angeles Times

Fannie Mae and Freddie Mac Unemployment Forbearance program. Fannie Mae and Freddie Mac have enhanced their Unemployment Forbearance program for homeowners who have lost their jobs. It is a proactive approach that is offered to the unemployed who are struggling with keeping up with their home loan payments.

What's Ahead For Mortgage Rates This Week : February 4 ...

FHLMC Seller Servicer Guide Vol 1 37.13 ( V ) Re-Entering the workforce For a borrower who re-entering the workforce and has less than a two-year employment and income history, the borrower's income may be qualifying income if the borrower has been at the current employer for a minimum of six months and there is evidence of a previous ...

Dollar bills and coins for personal finance bloggers and entrepreneurs.

Need Help? Please contact your Freddie Mac Account Representative or the Customer Support Contact Center. +1-800-FREDDIE. Start Cobrowse Session.

This Week's Stock Market News 4-19-2021

Conventional Loan 3% Down Available Via Fannie Mae & Freddie Mac April 8, 2015 - 7 min read Low-down-payment mortgage options: 3% down mortgages for first-time home buyers March 11, 2021 - 10 min read

Unemployment Letter To Mortgage Company - Unemployment ...

Proof of receipt of unemployment compensation for the most recent two years (IRS 1099-G(s) or equivalent. May not use unemployment if not received for two years. Temporary Help Services following: I613.BB Borrowers who work for a contract firm or temporary staffing firm may have stable income with all of the

5.2 million more seek unemployment aid — bringing four ...

01.09.2021 · which may require updated income documentation, before proceeding with using the income for qualifying. It is also recommended that, if possible, the Seller ask the employer during employment verification whether the borrower’s employment status or income level has changed within the last 60 days, as it is possible that a 10-day PCV employment

A twenty-four year old woman counting dollar bills.

For the purposes of determining stable monthly income, fluctuating additional employed income earnings are considered to be earnings that fluctuate on a regular basis, often based on factors such as hours worked, job type and performance. Fluctuating earnings may include, but are not limited to, income types such as commissions, overtime, bonus, tips, Reserve and National …

All should expect outsize economic volatility ahead ...

guidance for the analysis and treatment of income for self-employed Borrowers as described in Chapters 5304 and 5305 2The Seller must determine that the total stable monthly income meets the requirements and guidance for the determination of stable monthly income in Topic 5300. This includes, but is not limited to, business review and analysis

Looking Back and Looking Forward: The Macroeconomic Outlook

Seasonal income must be documented by obtaining the following: the borrower's recent paystub and IRS W-2 forms covering the most recent two-year period. (Signed federal income tax returns may also be required to verify unemployment income related to seasonal employment.) A verbal VOE is also required from each employer.

The Only Thing That Can Stop a Double Dip | The Fiscal Times

Homebuyers can now qualify for FHA Loans After Unemployment and gaps in employment. However, most lenders will require a 30 days paycheck stubs for the borrower to be able to close on their loan. Borrowers can have gaps in employment in the past two years and change careers to a different field and qualify for a mortgage.

Home Loan Forbearance Inches Up In Last Week of May | The ...

Unemployment income must be documented for two years, and there must be reasonable assurance that this income will continue. This requirement may apply to seasonal employment. Reference: For information on analyzing income from seasonal employment, see HUD 4155.1.4.D.2.e. 4155.1 4.E.3.d

Is Unemployment Income Considered Earned Income Law

Evaluating Income Amid a Pandemic. The coronavirus (COVID-19) global pandemic is challenging some potential borrowers and recent employment trends have complicated the qualifying process for borrowers who are experiencing temporary job loss because of COVID-19. Lenders have had to quickly adapt how they work with current and future homeowners ...

Unemployment Application Louisville Ky - YUNEMPLO

The Borrower's earnings may be comprised of base non-fluctuating earnings, ... When unemployment income associated with the seasonal employment is being ...

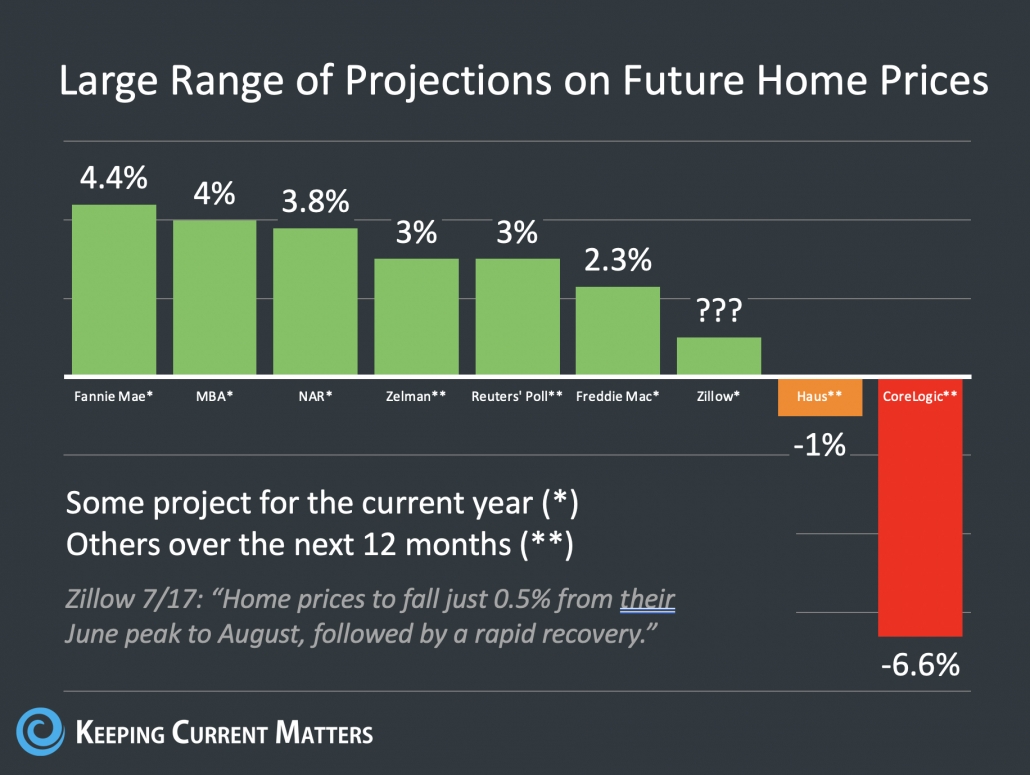

Housing Prices Set to Fall In 2021 | Shop Your Own Mortgage

Finance News of the Week 4-12-2021

Is Unemployment Income Taxable? - Communication Federal ...

Freddie Gray case explainer - Los Angeles Times

These Are the Top Slides to Share to Build Seller ...

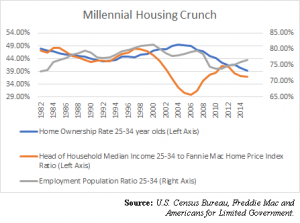

Millennial housing crunch underscores urgent need for ...

Polish Zloty (PLN)

FICO Scores Jump to 3-Year High - Saldutti Law Group

Money Money

Polish Zloty (PLN)

Average mortgage rates drop as rhetoric over China heats ...

The Aquarian Agrarian: Inflation-Adjusted Minimum Wage vs ...

Judge orders Freddie Gray hospital records turned over ...

300

This Week's Stock Market News 4-19-2021

Bowyer: The Problem with Affirmative Action Mortgages

Grave Employment Report - MBA Chart of the Week - Mortgage ...

Research Reveals Surprising Link Between Homeownership ...

Association of Industry Analytics - Economics

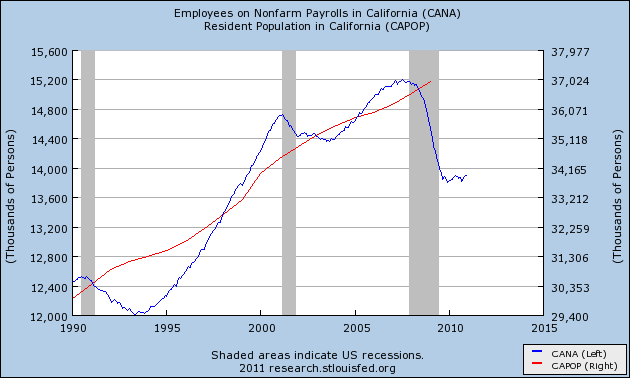

Is California the new Japan? - 5 charts showing nonfarm ...

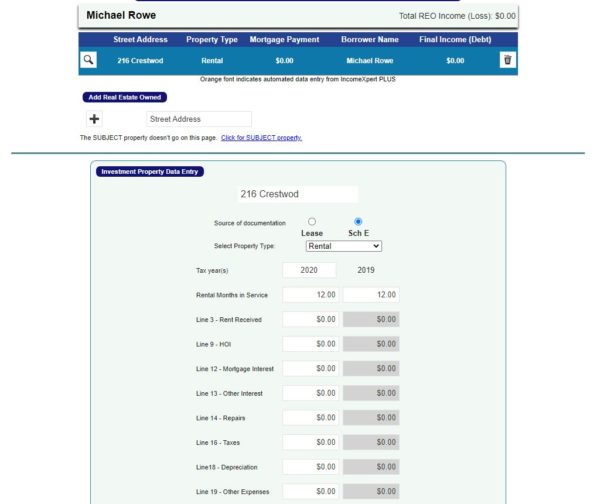

IncomeXpert - Blueprint

Lecture 12 Monetary Policy | Intermediate Macroeconomics

Lecture 12 Monetary Policy | Intermediate Macroeconomics

0 Response to "42 fhlmc unemployment income"

Post a Comment